A few days ago, Beijing Jianguang Asset Management Co., Ltd., Lianxin Technology, Qualcomm, and Beijing Zhilu Asset Management Co., Ltd. jointly signed an agreement to establish JLQ Technology, a joint venture company. The joint venture will focus on the design, packaging, testing, customer support, and sales of mass-market-oriented smart phone chipsets designed and sold in China.

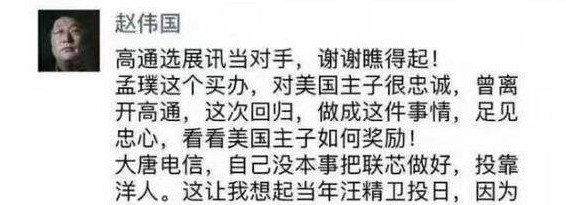

However, what the industry did not think of was that the incident triggered Tsinghua Unisplendid's irony. What is even more shocking is that Zhao Weiguo, Chairman of Ziguang Group, personally issued a report and claimed that Meng Qiao, the CEO of Qualcomm in this cooperation, was a comprador, and Lianxin was relying on foreigners.

So what exactly could have caused Zhao Weiguo, the chip industry in China, and even the global chip industry, to call it the “hungry tiger†(because the names of the chipmakers who were acquired by the crazy mergers and acquisitions) personally issued a document and even bombarded them with regard to individuals? attack?

Some analysts believe that the direct target of the research after the establishment of Hansun Technology is the exhibition news of Tsinghua Unisplendour. Such an analysis is not without reason. From the perspective of the focus area after the establishment of Hansheng Technology, the current situation is mainly based on low-end mobile phone chips. , may later in the field of the Internet of things chip force.

Spreadtrum’s current market positioning is basically based on mid-to-low-end mobile phone chips, although it has already begun to enter the mid-to-high end, that is to say, the establishment of Weisheng Technology has allowed Spreadtrum to add an opponent in the mobile phone chip market virtually. MediaTek challenged Qualcomm to face setbacks in the high-end mobile phone chip market. It recently claimed that it would put its focus back on the low-end market. The pressure on Spreadtrum’s information can be imagined.

However, then again, the strength and status of Spreadtrum’s low-end and mid-range mobile phone chips far exceeds that of Haosheng Technology (mainly the fourth largest shareholder of Lianxin Technology). According to our understanding, the current design level of Zeng Rui's chip has reached 16/14 nanometers. One quarter of the world's mobile phones have adopted Spreadtrum’s chips. Its chip shipments in 2016 have reached 600 million units, and the sales volume is 120. Billion, ranking 9th among global IC design companies.

On the baseband chip, Spreadtrum and Qualcomm and MediaTek are three points apart, with a market share of 27% in 2016. Why is Zhao Wei so angry? What's more, more than one opponent is beneficial from the perspective of business competition and diversification of market users. This has to make us think that perhaps the real crux is not here.

So we focused our attention on the pure capital behind Fusheng Technology: Jianguang Assets and Zhilu Capital.

In this cooperation, Jianguang (Gui'an New District) Semiconductor Industry Investment Center (Limited Partnership) contributed approximately 1.03 billion yuan in cash to the joint venture company, accounting for 34.643% of the registered capital of the joint venture company, and was the largest shareholder; Zhilu (Gui'an New District) The Strategic Emerging Industry Investment Center (Limited Partnership) contributed approximately RMB 510 million to the joint venture company in cash, which accounted for 17.091% of the registered capital of the joint venture company. The fourth largest shareholder. Perhaps the industry is relatively unfamiliar with these two companies. In fact, in the chip field, these two investment companies have long been famous.

For example, in February of this year, Jianguang Asset and Zhiluo Capital joined forces to purchase NXP’s standard parts business for US$2.75 billion. This is also the largest overseas M&A case in China’s semiconductor industry and shakes the industry. As early as 2015, Jianguang Asset successfully acquired NXP’s RF Power division for US$1.8 billion, and also jointly held a bipolar power component company Ruinen Semiconductor with NXP.

According to another source, Jianguang Assets is a holding company of China Construction Investment Corporation. Its main investment direction is high-tech industries. Through investments in recent years, Jianguang Assets has formed a sound layout in the semiconductor industry, from materials, equipment, and design. Manufacturing, packaging and testing all-embracing, allegedly currently the global semiconductor 1 / 3 of the products have their holding company figure, as Chi Road Capital, which has a global financial and industrial ecological chain resources.

I do not know what the industry feels like here? We believe that Jianguang Assets + Zhilu Capital (capital part) + Qisheng Technology (mainly the entity part of Lianxin Technology) is equivalent to Tsinghua Unisplendour (Capital) + Spreadtrum (physical part). The number of roads between the two sides is almost the same, both in terms of capital layout and supplemented by entities in order to seek the right to speak in the chip industry in China and even in the world. Especially in the Chinese chip market, as a result of gaining the right to speak, it is possible to obtain support (including subsidies) from state funds, at least from state-owned banks or financial institutions to enjoy preferential and preferential loans.

From this point of view, if Tsinghua Unisplendour, formerly known as the "national team" of chips, is favored by the national and national funds, then the future as an entity, if it can really be on the low-end chip market for Spreadtrum. As a threat, Qualcomm's role in assisting Corecore is particularly important, and Zhao Weiguo’s inability to directly attack Qualcomm’s Chinese CEO Meng Wei is the main reason. Even if it is to seize part of the market share, it will generate capital for Tsinghua Unisplendour’s capital operation. influences.

It is worth mentioning that in view of the high-profile and large-scale mad mergers and acquisitions before Tsinghua Unisplendour, foreign institutions and companies have already been highly vigilant against Violet. In the future, mergers and acquisitions-led capital operations are likely to encounter resistance. Jianguang Assets and Zhi Lun Capital acted in a low-key manner, with precision and efficiency in M&A and with great foresight. The timing was already higher than that of Tsinghua Unisplendour. (The acquisition of NXP’s RF Power unit was based on the use of NXP’s acquisition of Freescale. Opportunities that may trigger antitrust investigations are decisive.

With the complementarity of its two resources, it is very likely to replace Tsinghua Unisplendour's role in the Chinese chip industry. This is Zhao Weiguo’s fear and fear.

In the end, we would like to add that Zhao Weiguo, Chairman of Tsinghua Unisplendour Group, personally issued a document to bombard Suntech, and it is extremely unprofessional in terms of public relations and content. For example, it is said that Meng Tong, a Qualcomm Chinese CEO, is a comprador and is very loyal to the American master... But what we want to say is that as a professional manager affiliated with a global subsidiary, without compromising or violating China’s national interests and laws, For the company to maximize the benefits of professional managers is the most basic professional ethics.

As for the fact that Datang Telecom (the parent company of Lianxin Technology) does not have the ability to make Lianxin well-respected foreigners, it even ignores the facts. Not to mention the company's established Shengsheng Technology, Chinese owned 76% of the shares and has absolute control, if only the introduction of foreign capital is to rely on foreigners, then Tsinghua Unisplendour's Spreadtrum accepted Intel's 9 billion yuan What is the investment and the capital contribution for 20% of the shares?

To sum up, when “mutual tearing†has become the only means of competition among many industries and manufacturers in China, which hinders innovation and confuses the facts, the basic chip industry that our country has high hopes for has always been a pure land. However, China’s current chips need not only practical players such as Spreadtrum and Lianxin Technology (through innovative products to meet the needs of the market and users, to create their own brand image in the global chip industry), but also need to be like Qinghua Ziguang and Jianguang Assets. Chih-Ling Capital is well-versed in mastering capital operations to obtain more funds (after all, the chip industry needs super-high investment), and accelerates development and narrowing the distance with foreign chip industries through mergers and acquisitions and cooperation.

However, whether it is practical work or capital operation, we need to stand in the perspective of fair competition, and we must discourage the interference of non-market competition factors. Only in this way will our related companies abandon the interests of individuals and meet the country’s expectations and funding. Overtaking at the corner of the chip industry.