The global IaaS public cloud landscape has been set, AWS is far ahead, and Azure Google can only be in the second group. The domestic public cloud pattern is also basically stereotyped. Alibaba is far ahead, Azure, AWS, Penguin and so on are basically in the second group, and the public cloud itself has the attributes of the Internet business, which is in line with the characteristics of the winner, and when the leader forms the scale effect, The chaser often spends a lot of effort.

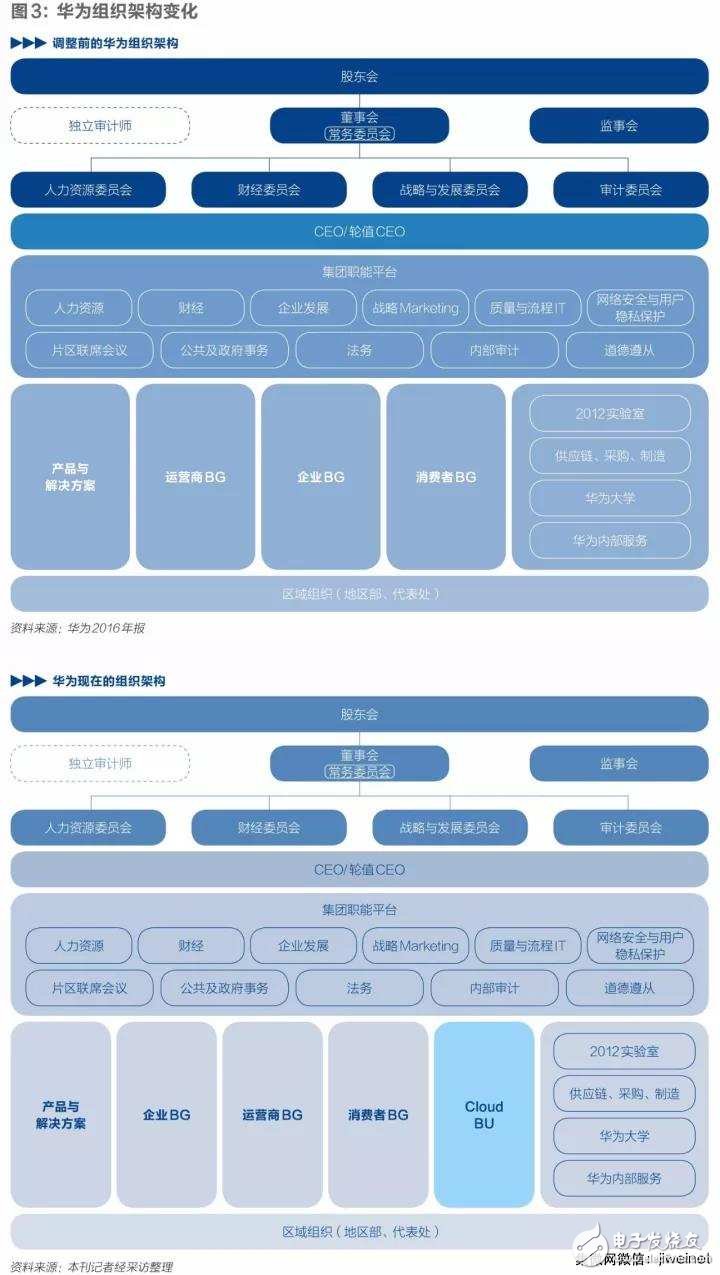

In August of this year, Huawei announced that Cloud BU has been upgraded to a first-tier department, which is in line with Huawei's original three major business group (BG) operators BG, consumer BG, and enterprise BG.

In September, Huawei’s rotating CEO Guo Ping announced the goal of Huawei’s public cloud business – there will be only five clouds left in the world, and Huawei will be “one of themâ€. Huawei has also set a phased goal - to become the top three in China's public cloud market in the next three years.

However, Huawei’s entry into the public cloud market is not a temporary rise. The reporter was informed that Huawei had quietly laid out the public cloud as early as 2011. It was only under the constraints of the existing business that Huawei’s decision-making layer was uncertain about whether it would be a public cloud or a public cloud.

"End pipe cloud" is a strategy repeatedly reiterated by Ren Zhengfei. The mobile phone is the "end", the telecommunication equipment is the "pipe", and the "cloud" is in the semi-absent state.

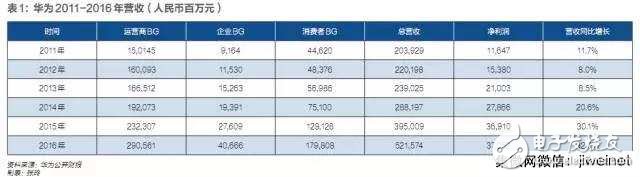

Huawei has been in the forefront in recent years. The telecommunications equipment business that has started is the world's number one, and the world's top three smartphones. The relatively weak one is the enterprise business. This BG is designed to provide IT solutions for enterprise customers. To the first camp in the world. In 2016, Huawei's revenue structure was 55.7% for operators, 34.5% for consumer business, and 7.8% for corporate business.

Huawei's enterprise BG has a private cloud business, and its development is good, but the industry trend has become obvious. Compared with the private cloud with scattered market and insufficient overall demand, the public cloud is the future of the cloud. At present, the market for “end†and “pipe†has reached the ceiling. Only when it is a public cloud, Huawei’s “cloud-end†strategy can form a closed loop and form a new growth pole. On the contrary, Huawei's growth will be stagnant.

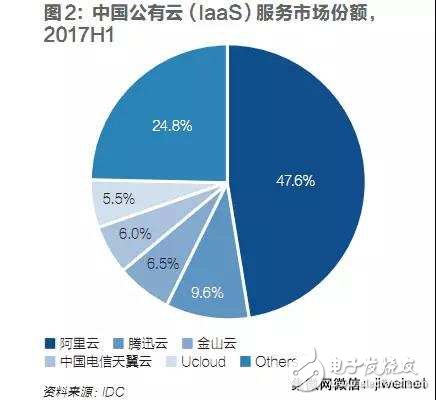

In every field that Huawei has entered in the past, there have been giants in control, and public clouds are no exception. Market consulting firm IDC data shows that as of the first half of 2017, the top five public cloud vendors in the world are Amazon AWS, Microsoft Azure, Alibaba Cloud, Google and IBM, of which AWS accounted for 45.4% and Ali cloud share was 4.5%.

Huawei's layout of public cloud services actually began in 2011, but Huawei once did not mention this business.

In 2011, Huawei, which intends to cut into the public cloud, smashed a “big bargainâ€: nearly 40 cloud computing experts including the CEO and CIO Jiang Jianping, who are the experts, are public clouds in China. Seed type experts in the field.

Cloud Express is the second company in the country to provide public cloud IaaS (infrastructure as a service). It was originally a subsidiary of Beijing Century Internet Broadband Data Center Co., Ltd. (NASDAQ: VENT, hereinafter referred to as "Century Internet"), but Century Internet divested the business before going public in the US, and the two became brother companies. Century Internet is not suitable for the "blood transfusion" of the cloud express line, and there are some contradictions in the distribution of management benefits, and the cloud fast line business has stagnated.

Two former core employees of the Cloud Express told reporters that Huawei originally intended to acquire the Cloud Express line as a whole, but did not talk to the Century Internet. In the end, due to the internal contradiction between the Century Internet and the Cloud Express, the Cloud Express The core employees are almost “one-stop†and do things at the lowest cost.

However, Huawei did not immediately set up a public cloud department, but placed the person in the "Internet" department of Huawei at the time called "Other BG."

In the Huawei organization structure in 2011, there was a business group called “Other BGâ€, and Huawei put some emerging businesses under this BG. Between 2009 and 2011, Huawei intends to enter the Internet market, so it recruited and established the "Internet" department.

The Internet department was later split into two. The 2C business was transferred to Huawei's terminal department. The cloud fast line team and 2B's business stayed. The department name was changed to Huawei Enterprise Cloud. At the same time, the number of employees increased to more than 200, and it remained at 2015. This scale.

The Huawei public cloud team was formed in a few months, and completed the core research and development of the public cloud platform. A core employee involved in research and development at that time told reporters that the speed of research and development is so fast, mainly because Huawei started server virtualization technology development in 2007, and has a mature virtualization solution (virtualization technology is one of the core technologies of cloud platform). ), coupled with the recruitment of experts from the cloud fast line has a wealth of public cloud research and development technology and experience.

The public cloud platform has been made, but what about doing public cloud business? This needs to be considered by the Huawei Strategic Development Committee.

A core employee of Huawei's public cloud team told reporters that at that time, Huawei had a great disagreement on whether to do public or not. In the end, the negative opinions prevailed. Only Xu Zhijun of Huawei's three rotating CEOs insisted on public cloud.

Huawei has three rotating CEOs, namely Xu Zhijun, Guo Ping and Hu Houkun. Among them, Xu Zhijun manages "things" (ie business), Guo Ping manages "financial", and Hu Houkun manages "people", which is equivalent to the separation of powers.

The core objection is that the public cloud is the owner's reserved land, and the operator is Huawei's largest source of revenue. Huawei cannot have business conflicts with operators.

Since 2010, the three major operators in China have successively deployed public clouds. China Unicom has also established a special cloud computing subsidiary. Huawei, as a communication equipment provider, adheres to the bottom line of not participating in “operations†and does not touch data, especially Touch communication data.

More critically, the three major domestic operators contribute tens of billions of yuan in revenue to Huawei each year. The total revenue of China's public cloud market until 2016 is only 10 billion yuan.

Another reason for being rejected is that the public cloud was considered to be aimed at a large number of small and medium-sized users. Each single business may be as low as 1,000 yuan, which is a “sweeping street†business; Huawei is good at “big businessâ€. The amount of each single business is mostly 10 million or even 100 million yuan. At that time, Huawei's entire organizational process, business model, skill reserve, and employee mentality were all different from those of the public cloud market.

This is not a good business as measured by financial indicators. Public cloud investment is a “swallowing gold beastâ€. To be successful in scale, Huawei is still a light asset operation as a device manufacturer and developer. The business of heavy asset investment has always been cautious.

Despite this, the cloud as an emerging IT trend makes it difficult for opponents to chop off this business, and Huawei's public cloud business barely retains.

This has created a peculiar situation. There is no public cloud department in Huawei's organizational structure, but more than 200 people have been doing public cloud business and become an invisible organization within Huawei.

Around June 2012, Huawei's first-generation public cloud platform was silently launched, mainly providing computing and storage-like cloud services. Like Amazon AWS and Alibaba Cloud, it is a true public cloud. This platform has never been publicized, mainly serving Huawei's own business department, but has gradually accumulated some external users.

In the first three years of low-key operation, the biggest contribution of public cloud business to Huawei is not revenue, nor how many users have accumulated. It is to help Huawei build business processes for public cloud users. Huawei did not have the experience, awareness and process of serving SME users before, and the public cloud took the first step.

“Cloud customers pay attention to the experience. If you are dissatisfied with you, you have to refund the money. Huawei is unbelievable about the money refund. The cloud business is small, and the financial department is at a loss. It took a long time to take it. These processes are established." A former Huawei public cloud business employee told reporters.

Until 2015, the invisible state of Huawei's public cloud business was terminated. In July of that year, Huawei released a public cloud platform called “Huawei Enterprise Cloud†for the Chinese market.

The new public cloud platform is Huawei's second-generation public cloud platform. It is based on the open source cloud computing framework OpenStack. Huawei is a platinum member of the well-known open source organization OpenStack.

At that time, a project insider told reporters that in order to avoid conflicts with operators, Huawei's claim to operators is that the platform can better provide public cloud solutions for operators.

Upgrade to core businessIn 2016, Huawei further upgraded its cloud strategy and proposed that Huawei's enterprise cloud should reach the order of 10 billion US dollars in 2020.

However, at that time, Huawei's enterprise cloud concept was broad-based, not specifically for public clouds, but also for the construction of joint venture clouds for operators and hybrid clouds for enterprises. At this time, Huawei still avoids the use of the term "public cloud."

It was not until March 2017 that Xu Zhijun announced at the Partner Conference that he would “strongly invest in creating an open public cloud platform†and increase the number of people in the business by 2,000 in the coming year.

This is the first time Huawei has publicly stated that it is going to be a "public cloud."

Public cloud as the main form of next-generation IT has become an indisputable fact. Major traditional IT giants including IBM, Microsoft, and Oracle have already started transformation. The process is difficult but firm.

Huawei's enterprise BG trades traditional IT business, and the external winds are under tremendous pressure on Huawei. At the end of 2016, Alibaba Cloud has defeated Google, second only to Amazon AWS and Microsoft Azure. This growth rate makes other public cloud players both amazed and anxious.

At the same time, AI has quickly become a slogan in the past two years. Public cloud can provide massive data and powerful computing power for AI. Grasping the public cloud has the hope of grasping the upstream position of the industrial chain in the AI ​​era.

A number of industry experts told reporters that in China, for entrepreneurial companies, the public cloud time window has been closed; for giant players, there are still 3 to 5 years.

In other words, if Huawei does not seize the public cloud, it will completely miss the opportunity to enter.

On August 28 this year, Huawei issued an internal document to announce the restructuring of the heavyweight organization. Cloud BU was promoted to the first-level department and was mainly responsible for the operation of the public cloud. The adjusted Cloud BU is level with Huawei operator BG, enterprise BG and consumer BG.

Cloud BU, which becomes a Tier 1 department, will have its own HR department, CTO office, strategy and business development department and financial management department. Starting this year, Cloud BU's revenue will also appear in Huawei's annual report. In September, Huawei announced its goal - there are only five clouds in the world, and Huawei has to do one of them.

At this point, the public cloud in Huawei from the invisible business that can not be obtained from the official name leap to the company's core business.

A middle-level supervisor who has worked for Huawei for more than 10 years told reporters that although Huawei is not a listed company, it needs high-growth business to maintain the stable operation of its internal share mechanism. The current three major businesses may face insufficient growth momentum or have Touching the apex of the industry, it is urgent to find the next high-growth business.

Since 2006, Huawei has announced annual revenue data. According to the annual report, Huawei's revenue increased from 39.7 billion yuan in 2005 to 521.6 billion yuan in 2016. During the period of 2012 and 2013 alone, the growth rate fell below 10%. In 2016, there was no increase in revenue. Many industry insiders predict that in the next three years, Huawei will continue to maintain the trend of increasing revenue without increasing profits.

Huawei is involved in three major markets: the carrier market, the enterprise IT market, and the consumer-facing personal terminal market.

Among them, Huawei's operator business has achieved its head position. In 2016, its revenue reached 290.6 billion yuan (about 43.7 billion US dollars), far exceeding the international competitor Ericsson (2016 revenue of 26 billion US dollars), but the 5G market is going to It is only possible to arrive around 2020, and it is currently in the gap period of 4G to 5G transition.

Although Huawei's smartphone sales have squeezed into the top three in the world, its profits are very low. More than 80% of the profits in the global smartphone market have been captured by Apple. Huawei has adjusted its strategy from a focus on value to a profit.

In the enterprise IT market, Huawei's BG revenue in 2016 was 40.7 billion yuan. Its business scale and brand influence have surpassed other local IT vendors, but compared with foreign established technology companies such as IBM, Hewlett-Packard, Dell, and Cisco. The big gap, and public cloud has been eroding the traditional IT market. According to Gartner data, global public cloud spending in 2016 has already accounted for 6% of total IT spending.

Right and left handsHuawei has been arguing with the interests of telecom operators, and has seen new changes in these years.

The biggest change is that the operator's public cloud strategy has largely failed globally. The US public cloud market is the most mature, but US carriers Verizon, AT&T and CenturyLink have closed public cloud services, and some even the basic cloud data centers are being sold.

In China's public cloud market, according to IDC data, only China Telecom's Tianyi Cloud is the best, and its market share ranks fourth. China Unicom's public Yunwoyun has been squeezed out of the top five. China Mobile's public cloud is responsible for each provincial company. This mechanism determines that China Mobile’s public cloud is difficult to grow.

Moreover, operators in the public cloud market actually win the role of "pipeline", not good at platform operations and services. Next, it is difficult for operators to compete with cloud services platforms such as Alibaba Cloud and Tencent Cloud. Based on this, many operators told reporters that they are not optimistic about the long-term development of public cloud business of Chinese operators.

"Since the mind knows nothing but Aliyun, Huawei wants to do it and let it do it," a Chinese telecom cloud computing expert told reporters.

The aforementioned Huawei public cloud team experts told reporters that in recent years, different operators have different attitudes toward Huawei's public cloud in different time periods. "China Unicom's opposition is fierce, because it has its own cloud company, the telecom mobile mentality is relatively peaceful, and the more it can accept this incident," he said.

Another important reason is that Huawei did not bypass the telecom operators when it opened up the public cloud market. Instead, it was deeply tied up and the two sides reached a tacit agreement.

In the cooperation between the two parties, Huawei provides cloud computing technology and customer service capabilities. Operators have rich customer resources and communication resources, which complement each other. In the face of customers, Huawei and the carrier team often co-exist and jointly fight.

Zheng Yelai, president of Huawei Cloud BU, said recently that Huawei's Cloud BU business includes Huawei's own public cloud and China Telecom Tianyi Cloud, as well as a cloud that cooperates with three foreign operators.

Despite this, a senior operator told reporters that after Huawei's large-scale deployment of public clouds, the relationship with operators has become complicated and subtle.

In the past, operators and Huawei were purely A-Party relations, but now, Huawei has become the operator of some operators on certain occasions. The embarrassing thing is that it is not a party with high bargaining power in front of operators.

A Huawei cloud business unit said that building a public cloud requires renting the operator's equipment room and bandwidth resources. However, Huawei's bargaining power in front of operators is not strong. The reason is that on telecommunications equipment, operators are big buyers of Huawei. .

One of the key considerations for Huawei to deploy its first public cloud node in Langfang, Hebei, was that Huawei’s carrier business in Langfang was generally done.

What is even more difficult to avoid is that the goal of Huawei's public cloud is the first camp in China, and it will inevitably face competition from the public cloud of operators. At that time, it is a dilemma for Huawei to continue to compromise on the existing carrier business for the public cloud or for the operator business.

Huawei has already experienced this dilemma of "left and right hands and hands". A Chinese telecom cloud computing person told reporters that Huawei Cloud and Telecom Tianyi Cloud had jointly bid for a cloud computing project of a car company. Huawei cloud quotes were much lower than Tianyiyun, which made a certain high-level person of China Telecom annoyed. Call Huawei-related executives to express their dissatisfaction.

Can you sell good products for sale?IDC statistics show that in 2016, China's public cloud IaaS market scale was 10 billion yuan, China's overall IT spending reached 2.3 trillion yuan (Gartner data), public cloud accounted for only 0.4%, which shows that China's public cloud market is still very At the beginning, as long as the strategy is right, Huawei has enough room for growth.

Ucloud founder and CEO Ji Yuhua commented that Huawei has both technical strength and strong capital, and is a company with both strategic determination and strong execution. Although the opportunity to break into the top three in China for three years is not big, in the long run, It is possible to become the main player of the public cloud. Ucloud is the fifth public cloud service provider in China.

Huawei has accumulated a lot of "teeth" over the years. Compared with other competitors, it has a complete IT product system from chip to server to storage to network, and also controls CT products and technologies, which enables Huawei to build a cost-effective cloud infrastructure, and it has a large platform development system and The 2012 lab provides long-term technical support.

However, Huawei also faces multiple challenges, and some of them are still not faced by the opponents.

One challenge is that Huawei must first “genetically transform†itself into a public cloud.

From CT to IT to consumer-grade terminals, Huawei specializes in R&D and production of various devices, but public cloud sells services. Currently, successful public cloud vendors, except Microsoft, are service-originated Internet vendors. Zheng Yelai has publicly stated on many occasions that Huawei needs to change from selling equipment to selling goods.

But this is not easy. Huawei is a product company. It has been so successful in the past because the entire R&D process, management, sales and service systems are born for the product and have solidified into its corporate culture.

For example, Huawei strictly adheres to the Integrated Product Development (IPD) process in research and development. The IPD process helps to develop highly reliable equipment. It needs to be approved by the leader every step of the way, and it is especially suitable for the development of communication equipment products with high standardization, relatively stable demand and high quality requirements.

Cloud services are different. Cloud customers vary widely and demand varies. Therefore, R&D and operation are required to be closely integrated, and rapid iterative development is required to quickly respond to the personalized needs of the front-end.

Huawei itself is clearly aware of this.

The reporter was informed that Huawei Cloud BU was given the privilege: it does not need to comply with Huawei IPD and other processes, but it takes time to explore a R&D, service and sales system suitable for public cloud.

Moreover, the already formed thinking inertia is more difficult to reverse. A Huawei person commented that Huawei is still thinking about cloud or product thinking, not service thinking. It is not always about what users want, but always consider what products I can offer.

Another important thing at the moment is that Huawei urgently needs to find a number of benchmark users.

When Alibaba Cloud, Tencent Cloud and Jinshan Cloud started their homes, they surrounded a group of seed users based on their respective Internet businesses.

For example, Alibaba Cloud not only has a large number of small and micro enterprises or even individual users, but also a super application such as “Double Elevenâ€; Tencent Cloud has the support of game developers – for game developers, if they want to be listed in Tencent game applications The leaderboard, an unwritten but well-known method, is to use Tencent Cloud; Jinshan Cloud's early user accumulation also depends on the support of Jinshan Games and Xiaomi Ecology.

Although these users are mainly small and medium-sized enterprises, they are extremely beneficial to the early development of public cloud vendors.

Jinshanyun, an operations director, told reporters that public cloud emphasizes starting from small customers, accumulating a large number of universal reliable and maintainable operational experience from unreliable services that small customers can afford, and gradually shifting from a large number of manual operation services to automation and refinement. Operation, and gradually improve the maturity and stability of the cloud platform, as well as the team's refined operation and maintenance capabilities, it is difficult to quickly fill up by rushing around or digging around.

Huawei's user base is just the opposite. It is dominated by large and medium-sized government and enterprise customers. However, for most government and enterprise users, the public cloud is more cautious, and the demand is not strong. If it is on the cloud, it is mostly a policy-oriented cloud. This kind of user is worth fighting for, but it is more difficult.

Zheng Yelai recently said in an interview with the media that today, almost all Internet applications are in the cloud, but the digital transformation of the government and enterprises has only just begun. This is Huawei's opportunity.

If Huawei's benchmark users are in the government and large enterprises, and the needs of large enterprises are diverse and complex, relying on Huawei's own efforts is difficult to do well, then ecological construction is very necessary.

For public cloud vendors, basic computing and storage cloud services are basic capabilities, anyone can do it, profits are very thin, whether PaaS (platform as a service), SaaS (software as a service) is rich, cloud industry Whether there are many partners is the key to the user and the main source of profit. This is the ecological construction of the public cloud.

Ji Yuhua commented that among the public cloud manufacturers, the best ecological construction is Alibaba Cloud. Moreover, Alibaba Cloud is strong in its ability to pay and big data, and other vendors are hard to find in this regard.

Huawei announced the "Cloud Partner Program 1.0" in the first half of this year.

According to the plan, Huawei Public Cloud will focus on developing and reselling Huawei's public cloud services (cloud resale partners), Huawei-based public cloud development applications (cloud solution providers), and responsible for migrating enterprise applications to Huawei's public cloud. Three types of partners (cloud service partners).

In addition, the public cloud is only "swallowing gold beasts." Liu Liming, a senior expert in cloud computing, told reporters that from the history of capital investment from Google, Microsoft and IBM, if you want to sprint the first echelon of public cloud, the annual investment in infrastructure needs to be 1 billion US dollars, and the investment in research and development operations is also 10 Billion dollars.

Even in Huawei, in the long run, such a scale of investment will make the capital chain tight. Huawei is not a listed company and cannot be financed from the secondary market. The return period of the public cloud is too long. Alibaba Cloud is still not profitable. This determination of Huawei is a test.

Zheng Yelai believes that if Huawei does not do cloud services, the current three major businesses (consumer business, carrier business and enterprise business) will have no base. At the same time, Huawei has invested in a complete investment from chip to system around the IT industry, but this market space is being squeezed step by step by the public cloud. Without the cloud service business, the return on investment for many years will be greatly reduced.

At the end of September, Zheng Yelai reported to the company's standing board that the public cloud future business plan was successfully passed. He told the team, "No one has any restrictions on the public cloud business."

8GPU B85-Pro Mining Rig(Black)

ETH/ETC/AE/BTM/GRIN/GRIN31/BEAM/SERO/RVN/MONA/CKB/XVG/BCD/FIRO/HYC/VTC/CLO/RVC/PGN/CHI etc.

Applicable graphics card: GPU P104,GPU P106,GPU 1660,GPU 3060,GPU 3070,GPU 3080,GPU 580,GPU 598, GPU 5600XT,GPU 5700XT

rig mining,mining rig for sale,ethereum mining rig,mining rig ethereum,ethereum mining rigs

Easy Electronic Technology Co.,Ltd , https://www.pcelectronicgroup.com